Department of Finance Canada

Tax Policy Branch

Tax Legislation Division

90 Elgin Street, Ottawa, ON K1A 0G5

Email: consultation-legislation@fin.gc.ca

Subject: Submission on Hybrid Mismatch Arrangements — Technical Comments and Recommendations

This submission sets out comments of the Joint Committee on Taxation of the Canadian Bar Association and Chartered Professional Accountants of Canada (“Joint Committee”) regarding the Hybrid mismatch arrangements, as proposed in the draft legislative proposals released on January 29, 2026.

Members of the Joint Committee and others in the tax community participated in the discussion concerning this submission and contributed to its preparation, including:

- Ian Bradley – PwC

- David Bunn – Deloitte

- Harry Chana – BDO Canada

- Nik Diksic – EY

- Richele Frank – KPMG

- Kaitlin Gray – Osler

- Hetal Kotecha – BDO Canada

- Daryl Maduke – BDO Canada

- Ryan Minor – CPA Canada

- Ken Saddington – Goodmans

- Jeffrey Shafer – Blakes

- Simon Townsend – RSM

- Sabrina Wong – KPMG

We would be pleased to discuss this submission with you in further detail at your convenience.

Yours truly,

Janette Pantry

Chair, Taxation Committee

Chartered Professional Accountants of Canada

Anu Nijhawan

Chair, Taxation Section

Canadian Bar Association

CC: Trevor McGowan, Associate Assistant Deputy Minister, Tax Policy Branch

Joint Committee on Taxation of The Canadian Bar Association and CPA Canada

Submission to the Department of Finance

Submission on Draft Legislative Proposals Released January 29, 2026

Hybrid Mismatch Arrangements — Technical Comments and Recommendations

The Joint Committee on Taxation of The Canadian Bar Association and CPA Canada (the “Joint Committee”) appreciates the opportunity to provide comments to the Department of Finance Canada on the draft legislative proposals released on January 29, 2026 (the “Proposals”). This submission focuses on the Proposals implementing additional elements of Canada’s hybrid mismatch regime, including the rules relating to hybrid payer arrangements, reverse hybrid arrangements, disregarded payment arrangements, and the related withholding tax consequences, as well as the accompanying definitional framework (including the “ordinary income” and “dual inclusion income” definitions).

We appreciate the policy objective of neutralizing hybrid mismatch outcomes in a manner consistent with the OECD BEPS Action 2 Report1 (“Action 2 Report”). At the same time, several aspects of the Proposals—as currently drafted—may produce outcomes that are difficult to administer, inconsistent with the Action 2 ordering and coordination principles, or disproportionate in circumstances where there is no material mismatch or where income is subject to full taxation in at least one jurisdiction. Our recommendations are intended to improve clarity and predictability, better align the technical rules with their policy intent, and reduce the risk of double taxation or unintended withholding tax exposure, including in common commercial structures (such as ordinary third-party financing arrangements).

For ease of reference, we have organized our comments by theme and included targeted recommendations in each section. We would welcome the opportunity to discuss these issues with the Department of Finance and to assist further as the Proposals are refined.

Dual Inclusion Income

The “dual inclusion income” and “investor dual inclusion income” concepts play a critical role in delineating the proper scope of the disregarded payment rules in subsections 18.4(15.3) to (15.4) and the hybrid payer rules in subsections 18.4(15.5) to (15.7).2 The terms “dual inclusion income” and “investor dual inclusion income”, and the supporting term “ordinary income”, must be carefully defined to prevent the hybrid mismatch rules from producing double taxation outcomes. The definitions of these terms should follow the guidance in the Action 2 Report, which carefully considered these issues.

Effects of Tax Relief

The “ordinary income” definition supports the “dual inclusion income” and “investor dual inclusion income” definitions, by describing the amounts that are considered to be included in ordinary income in respect of a country. The language used in the “ordinary income” definition appears to be based in part on the “Canadian ordinary income” and “foreign ordinary income” definitions in the currently enacted legislation. This causes some interpretive difficulties, as those definitions serve a different function.

Under paragraph (a) of the “ordinary income” definition, an amount is excluded from ordinary income in respect of a particular country to the extent that “the amount can reasonably be considered to be excluded, reduced, offset or otherwise effectively sheltered from the income or profits tax under the laws of that country by reason of any exemption, exclusion, deduction, credit (other than a credit for tax payable under Part XIII or for a tax that is substantially similar to tax under Part XIII) or other form of relief that applies specifically in respect of all or a portion of the amount and not in computing the entity’s income or profits in general” (Variable D). Similar language is used in the definitions of “Canadian ordinary income” and “foreign ordinary income”. However, the meaning of this exclusion in the context of the “ordinary income” definition is unclear, because that definition deals with all amounts that are included in computing income (rather than focusing on specific payments that receive hybrid tax treatments). The meaning of tax relief that “applies specifically in respect of all or a portion of an amount and not in computing the entity’s income or profits in general” is unclear in this context. The Explanatory Notes do not provide sufficient guidance on this point.

Recommendations: Clearer guidance should be provided on what forms of tax relief will prevent an amount from being included in ordinary income. This guidance could be provided through examples in the Explanatory Notes, although in some cases revisions to the “ordinary income” definition itself may provide greater clarity. We discuss below some specific scenarios for which clarification is particularly important.

Foreign Tax Credits

Where income of a hybrid payer is subject to tax in two countries, one country often grants a foreign tax credit for tax paid on the income in the other country. This can be illustrated by two simple examples:

- A U.S. corporation (“USCo”) holds an equity interest in a Canadian unlimited liability company (“ULC”) that is treated as fiscally transparent for U.S. tax purposes. ULC is subject to Canadian tax on its income. USCo is subject to U.S. tax on its share of ULC’s income, with a foreign tax credit provided in the U.S. for the Canadian tax paid on that income.

- A Canadian corporation (“Canco”) carries on business through a permanent establishment located in the U.K. Canco is subject to U.K. tax on the income attributable to this permanent establishment. Canco is also subject to Canadian tax on this income, with a foreign tax credit provided in Canada for the U.K. tax paid on the income.

The Action 2 Report states that “[d]ouble taxation relief, such as a domestic dividend exemption granted by the payer jurisdiction or a foreign tax credit granted by the payee jurisdiction should not prevent an item from being treated as dual inclusion income where the effect of such relief is simply to avoid subjecting the income to an additional layer of taxation in either jurisdiction”.3 This treatment reflects the overall goal of the hybrid mismatch rules: ensuring that income is subject to full taxation in one country, rather than taxing the same income in multiple countries.

The “ordinary income” definition in subsection 18.4(1) excludes an amount that is effectively sheltered from tax due to tax relief “that applies specifically in respect of all or a portion of an amount and not in computing the entity’s income or profits in general”. Tax credits provided for Part XIII taxes (or for substantially similar taxes) are expressly removed from the scope of this exclusion. There is no express carve-out for foreign tax credits that are provided for ordinary net income tax (such as the tax credits in the two scenarios discussed above).

Subsection 18.4(2) provides that the rules in section 18.4 are to be interpreted consistently with the Action 2 Report, unless the context otherwise requires. In this context, we believe an amount that is included in computing income that is subject to tax in a country will be considered ordinary income, notwithstanding that a foreign tax credit is provided for tax paid on that income in another country. We believe that the foreign tax credits provided under section 126, and similar foreign tax relief provided under the income tax laws of other countries, would be considered tax relief that applies in computing an entity’s income or profits in general (rather than relief that applies specifically to particular amounts). However, we believe that clarification on the treatment of such foreign tax relief would be helpful, to avoid confusion.

Recommendation: The “ordinary income” definition in subsection 18.4(1) (or the related Explanatory Notes) should clarify that double taxation relief, such as a foreign tax credit or similar foreign tax relief granted by a country in respect of taxes paid on an amount of income in another country, does not prevent that amount from being treated as ordinary income in respect of the first country.

Inter-corporate Dividends

Tax relief provided for inter-corporate dividends raises similar issues. Many countries provide deductions (or similar relief) for dividends received by a corporation from another corporation in certain circumstances, to achieve corporate integration and prevent the same income from being subjected to multiple levels of taxation. For example, subsection 112(1) provides a deduction for dividends received from taxable Canadian corporations, and subsection 113(1) provides deductions for dividends received from foreign affiliates (to the extent of certain tax attributes of the affiliates).

Intercorporate dividends that are eligible for such deductions might not be considered “ordinary income”, on the basis that these deductions are a “form of relief that applies specifically in respect of” the dividends. This seems inconsistent with the Action 2 Report, which as noted above, indicates that domestic dividend exemptions and foreign tax relief should not prevent dividends from being included in ordinary income, where such tax relief prevents the income from being subject to an additional layer of taxation in the hands of the dividend recipient.

This can be illustrated by an example involving a U.S.-resident corporation (“USCo”) that holds an equity interest in a Canadian ULC (“Canco 1”), which is treated as fiscally transparent for U.S. tax purposes. Canco 1 owns all of the shares of a Canadian corporation (“Canco 2”), which is treated as a separate entity for U.S. tax purposes. Canco 2 has $100 operating income, which is subject to Canadian tax, and pays a $75 dividend to Canco 1 (representing its after-tax income). The dividend is included in Canco 1’s taxable income, and an offsetting deduction is claimed under subsection 112(1). Canco also makes $10 payments for administrative expenses, which are deducted in computing its income for Canadian tax purposes. USCo includes its share of the dividend income received by Canco 1 and the administrative expenses incurred by Canco 1 in computing its income for U.S. tax purposes. If the dividend were excluded from Canco 1’s ordinary income due to the subsection 112(1) deduction, there would be no dual inclusion income, and the deduction of Canco 1’s expense payments would be denied as the amount of a hybrid payer mismatch under subsection 18.4(15.6). This seems like an inappropriate result, since the subsection 112(1) deduction merely reflects the fact that the income from which the dividend is paid is subject to Canadian tax in the hands of Canco 2.

We acknowledge that the definition of “Canadian ordinary income” in subsection 18.4(1) excludes dividends that are eligible for deductions under sections 112 or 113. However, this exclusion reflects the specific context of the “Canadian ordinary income” definition, which supports the “deduction / non-inclusion mismatch” test in subsection 18.4(6). Those rules address hybrid mismatch arrangements in which an amount is deductible in respect of the payment of a dividend, but the dividend is not taxed in the hands of the recipient. The “ordinary income” definition serves a different purpose: it merely determines whether amounts are included in the computation of income. If a particular amount represents a payment that is deductible by the payer, any potential hybrid mismatch relating to that deduction is properly addressed by the hybrid mismatch rules for deduction / non-inclusion mismatches, rather than the “ordinary income” and “dual inclusion income” concepts (which are used here to relieve the consequences of a double deduction).

Recommendation: The “ordinary income” definition in subsection 18.4(1) (or the related Explanatory Notes) should indicate that a dividend amount will not be excluded from ordinary income merely because that amount is eligible for a deduction under sections 112 or 113 (or similar tax relief that is provided for intercorporate dividends under foreign tax laws).

Trust Distributions

A Canadian-resident trust is generally entitled to a deduction in computing its income under subsection 104(6), to the extent that an amount of its income becomes payable to a beneficiary. Similar to the intercorporate dividend deductions noted above, the deduction under subsection 104(6) seeks to prevent income from being subject to multiple levels of tax. Unlike those deductions, the deduction under subsection 104(6) is claimed by the payer of a distribution, rather than the recipient. We believe that an amount of trust income would not be excluded from ordinary income merely because the trust distributes its income to its beneficiaries, and claims a deduction under subsection 104(6) in respect of the distribution. We believe the deduction under subsection 104(6) would be considered tax relief that applies in computing the trust’s income or profits in general, rather than relief that applies specifically in respect of particular income amounts. However, clarification would be helpful on this point, to avoid confusion.

Recommendation: The “ordinary income” definition in subsection 18.4(1) (or the related Explanatory Notes) should clarify that an amount of trust income will not be excluded from ordinary income merely because the trust receives a deduction under subsection 104(6) in respect of the distribution of that income to its beneficiaries.

Dual Inclusion Income Issues with Multiple Entities

The Proposals relieve taxpayers from the denial of a deduction under subsection 18.4(4) or the inclusion of income under section 12.7 in certain circumstances to the extent of dual inclusion income. However, the entity-by-entity definition of dual inclusion income creates the possibility of a mismatch between a deductible payment (without regard to the Proposals) and related income that should be treated as dual inclusion income. Examples of anomalies resulting from this entity-by-entity approach are provided below, along with recommendations to address these issues.

Examples Involving Multiple Fiscally-Transparent Entities

The following examples illustrate inappropriate results produced by the entity-by-entity approach to dual inclusion income, in contexts involving multiple hybrid entities in a country.

Example 1

Consider, for example, a U.S. corporation (“USCo”) that directly owns all of the shares of two Canadian ULCs (“ULC1” and “ULC2”), both of which are treated as fiscally transparent for U.S. tax purposes. ULC1 carries on business in Canada and earns income that is taxed in both Canada (in the hands of ULC1) and in the U.S. (in the hands of USCo). ULC2 is established for commercial purposes as a financing entity. ULC1 needs debt to finance its business, but for commercial purposes it is desirable for ULC2 to borrow the funds from unrelated third parties and on-lend the funds to ULC1. Payments of interest by ULC2 give rise to a hybrid payer arrangement, but because ULC1 and ULC2 are both disregarded for U.S. tax purposes, the inter-company payment of interest is not recognized for U.S. purposes and ULC2 has no dual-inclusion income of its own. There is Canadian income that is dual inclusion income that is effectively connected to the debt, earned by ULC1, but this income does not reduce the amount of the hybrid payer mismatch for ULC2 under proposed subsection 18.4(15.6) because it is not dual inclusion income of the hybrid payer (ULC2). Given the connection between ULC1’s business income and the borrowing, it would be appropriate for ULC2 to be able to recognize for purposes of subsection 18.4(15.6) dual inclusion income earned by ULC1.

Example 2

Consider a second example of a U.S. REIT (“USREIT”), which directly owns all of the shares of a Canadian corporation (“Canco”), which itself directly owns all of the shares of a Canadian subsidiary (“CanSub”). Both Canco and CanSub are “qualifying REIT subsidiaries” for U.S. tax purposes, and are thus disregarded for U.S. tax purposes. For commercial reasons the group structures a third-party borrowing as a borrowing by CanSub with an on-loan to Canco. As with the above example, interest paid by CanSub gives rise to a hybrid payer mismatch, but CanSub has no dual inclusion income of its own, while CanCo earns dual inclusion income but does not incur expenses giving rise to a double deduction (because the interest paid by Canco to CanSub is disregarded for US tax purposes). Given the connection between these entities, and especially because the “look-though” to CanSub for U.S. purposes relies on the simultaneous hybridity of Canco, it would be appropriate for CanSub to be able to recognize for purposes of subsection 18.4(15.6) the dual inclusion income earned by Canco.

Recommendations

- Revise the Proposals to allow the sharing of excess dual inclusion income among members of a corporate group. This approach has been implemented in the UK where, since 2021, dual inclusion income can be allocated among members of the same corporate group. This rule is specifically intended to mitigate the potential economic double taxation that can arise when the hybrid mismatch rules are applied to groups that have multiple hybrid entities.

- In the alternative, a more restrictive sharing approach could be allowed, under which an inter-company payment from a particular Canadian entity to a recipient Canadian entity within the same group could be considered to give rise to dual-inclusion income for the recipient entity (even if that would not otherwise be the case because, for example, the payment is disregarded in the other relevant jurisdiction as a payment between two hybrid entities) if the payment can reasonably be regarded as being funded from income in the particular entity that is taxed in Canada. This approach would be analogous to Australia’s “on-payment” rule.

- In the final alternative, consider expanding the discretion provided for in subsection 18.4(19.1) to permit the Minister, on a discretionary basis, to recognize dual inclusion income earned by related Canadian taxpayers in appropriate circumstances. This approach is not preferred, as the need for discretionary approval is an administrative burden and unnecessarily impairs consistency and predictability of the rules.

Controlled Foreign Company (CFC) Taxes

The “ordinary income” definition does not include amounts that are subject to tax under a controlled foreign company (“CFC”) tax regime (because CFC taxes are excluded from the amended “income or profits tax” definition in subsection 18.4(1)). Accordingly, an amount of income earned by an entity will not be included in dual inclusion income if the amount is included in computing the entity’s income for tax purposes in its country of residence, and is also included in CFC income that is subject to tax in an investor’s country.

This seems inconsistent with the Action 2 Report, which states that “[a] tax administration may treat the net income of a controlled foreign company that is attributed to a shareholder of that company under a CFC or other offshore inclusion regime as dual inclusion income if the taxpayer can satisfy the tax administration that the effect of the CFC regime is to bring such income into tax at the full rate under the laws of both jurisdictions”.4

This can be illustrated with the following example. A U.S. resident person (“US Investor”) owns all of the shares of a Canadian ULC (“Canco 1”), which is fiscally transparent for U.S. tax purposes. Canco 1 owns all of the shares of a Canadian corporation (“Canco 2”), which is treated as a separate entity for U.S. tax purposes. Canco 1 pays $50 of interest, which is deductible by Canco 1 for Canadian tax purposes and by US Investor for U.S. tax purposes. Canco 2 has $100 of property income, which is taxed in Canada; US Investor is also taxed on its share of this income under U.S. CFC tax rules (the subpart F rules).

Canco 1 is a hybrid entity, and the interest payments produce a double deduction mismatch. Canco 2’s property income is taxed in Canada and is also taxed under US CFC tax rules. However, this income would not be considered dual inclusion income, because US Investor is not considered to be subject to an income or profits tax on this income. Therefore, even though interest paid by Canco 1 is deductible by the US Investor and offsets the Subpart F income of the US Investor in respect, a similar offset is not possible when applying the hybrid payer rules to the interest expense.

As discussed above, the entity-by-entity approach to dual inclusion income should be replaced with a broader approach, consistent with the Action 2 Report. We believe this change should also address income that is subject to tax in two countries due to a CFC tax regime ( e.g., income earned by an entity that is not itself a hybrid entity, but whose income is subject to tax in an investor’s country under a CFC tax regime).

Recommendation: Dual inclusion income should include income that is subject to an ordinary income or profits tax in one country and is also subject to tax in an investor’s country under a CFC tax regime.

Inclusion / No-Deduction Payments

Anomalous results can also arise where an investor in a hybrid entity makes a payment to that entity, which is disregarded under the tax laws of the investor’s country. Although the payment is included in the hybrid entity’s ordinary income, it would not be dual inclusion income (because both the expense and revenue relating to the payment are disregarded under the investor country’s tax laws). The payment therefore produces an “inclusion / no-deduction” outcome (essentially the reverse of the “deduction / non-inclusion” mismatches targeted by the disregarded payment arrangement rules).

This anomaly can be illustrated by the following examples:

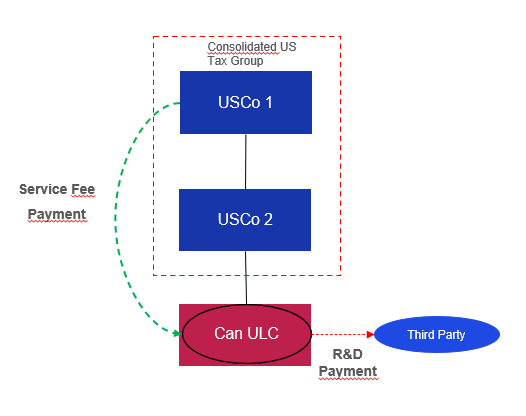

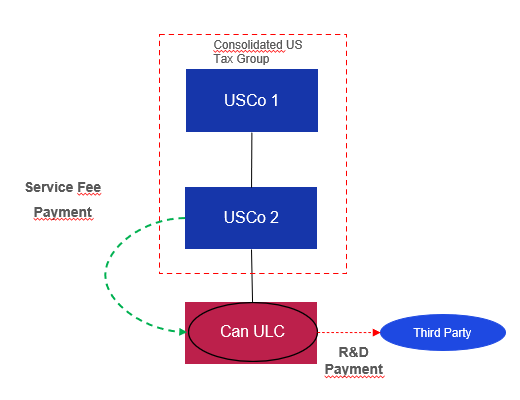

- Two US companies (“USCo 1” and “USCo 2”) are members of a consolidated group for U.S. tax purposes. USCo 1 owns all of the shares of USCo 2.

- USCo 1 owns all of the shares of a Canadian ULC (“Can ULC”), which is treated as fiscally transparent for U.S. tax purposes.

- Can ULC is a service provider to the U.S. group; it receives payments from members of the U.S. group for the performance of those services, and has no source of income aside from those service fees.

- Can ULC makes payments to arm’s length third parties for general expenses (for example, assuming Can ULC is performing R&D services, Can ULC’s expenditures include wages, direct and indirect costs, subcontracts, etc.).

- Can ULC earns an arm’s length margin and complies with the transfer pricing rules in section 247.

- For illustrative purposes, assume Can ULC receives $100 of service fee payments and makes a $90 R&D payment, such that Can ULC’s net profit is $10.

The application of the hybrid payer arrangement rules would vary significantly depending on whether the service fees are received from USCo 1 (the “grandparent” of Can ULC) or USCo 2 (the direct parent).

The “grandparent payment” scenario is illustrated below.

The conditions in subsection 18.4(15.5) would be satisfied in respect of the R&D payment. Can ULC is a Canadian-resident hybrid entity, and is therefore a hybrid payer. USCo 2 is an investor, who does not deal at arm’s length with Can ULC. For the purposes of this discussion, we assume that no foreign hybrid payer mismatch rule applies, in respect of the payment in computing the relevant foreign income or profits, for a foreign taxation year, of this investor. The R&D payment gives rise to a double deduction mismatch, since an amount is deductible in respect of the $90 payment in computing the income of both Can ULC and USCo 2. In the example, the double deduction mismatch is therefore $90.

The formula in subsection 18.4(15.6) computes the amount of the hybrid payer mismatch, as the amount of the double deduction mismatch in respect of the payment ($90) less the amount of dual inclusion income. In this example, the $100 service fee payment is received from USCo 1, and is included in computing the income of both Can ULC (for Canadian tax purposes) and USCo 1 (for U.S. tax purposes). The $100 “grandparent” payment is therefore dual inclusion income. Thus, the hybrid payer mismatch amount is nil in this scenario.

A “direct parent payment” scenario is illustrated below.

The conditions in subsection 18.4(15.5) are satisfied in respect of the R&D payment (for the same reasons discussed above). However, the treatment of the service fee is different. Where the service fee is paid by USCo 2 to Can ULC, USCo 2 does not have ordinary income in respect of this payment (no amount is included in computing its income or profits of the year) because the payment from Can ULC is disregarded for U.S. tax purposes. As a result, the payment is not dual inclusion income. Consequently, in this “direct parent payment” example, the amount of the hybrid payer mismatch under subsection 18.4(15.6) would be $90, notwithstanding that the economic result is the same as the “grandparent payment” example.

We note that the U.K. amended its hybrid mismatch rules to address such “inclusion / no-deduction” scenarios involving disregarded payments to hybrid entities. The U.K. rules essentially treat such payments as ordinary income of the investor, if the payment is non-deductible for the investor solely because the hybrid entity is viewed as fiscally transparent for tax purposes in the investor’s country.5

Recommendations:

- Consider adjusting the definition of “ordinary income” to deem a payment received by a hybrid entity to be ordinary income of an investor, where the payment is disregarded under the tax laws of the investor’s country (the U.K. approach discussed above could serve as a model).

- In the alternative, consider expanding the discretion provided for in subsection 18.4(19.1) to permit the Minister, on a discretionary basis, to recognize dual inclusion income earned by related Canadian taxpayers in this circumstance. As discussed elsewhere in these submissions, this approach is not preferred, as the need for discretionary approval is an administrative burden and unnecessarily impairs consistency and predictability of the rules.

Other Hybrid Payer Issues

Definition of a Hybrid Entity

The Action 2 Report describes a hybrid entity as an entity that is treated as “…a separate taxpayer in its jurisdiction of establishment but as transparent under the laws of its parent…”.

The hybrid entity concept is incorporated into the Proposals through the definition of “hybrid entity” in subsection 18.4(1). Specifically, a hybrid entity is defined under the proposed definition as an entity:

- that is resident in a country; and

- any portion of the income, profits, expenses or losses of which is treated, for income tax purposes under the laws of another country, as income, profits, expenses or losses of another entity that is resident in the other country (or would be so treated if there were any such income, profits, expenses or losses).

We are concerned that the language in paragraph (b) could potentially be interpreted in an overly broad and unintended way. For instance, assume “XCo”, a corporation resident in County X, owns all of the shares of “Canco”, a corporation resident in Canada. Canco earns $100 of active business income, and also earns $10 of passive interest income and incurs $5 of interest expense.

Under the laws of Country X, Canco is viewed as a separate corporation (i.e., Canco is not fiscally transparent under the laws of Country X). However, under the controlled foreign company (“CFC”) regime in Country X, the passive income and expenses of Canco are included in the taxable income of XCo.

We believe it is clear, based on the Action 2 Report, that Canco is not a hybrid entity by virtue of a portion of its income or expenses being included in the taxable income of XCo, unless it is due to Canco being fiscally transparent under the relevant foreign tax law. We also believe this is the appropriate way to interpret the existing language in the proposed definition of “hybrid entity” is subsection 18.4(1).

However, for greater certainty, and to ensure the hybrid entity definition is not applied in an overly broad and unintended way, we recommend that paragraph (b) of the “hybrid entity” definition be replaced with language similar to that used for the definition of “fiscally transparent” in subsection 2(1) of the Global Minimum Tax Act. For consistency, we recommend that paragraph (b) of the “investor” definition be revised in a similar way.

Recommendation:

We recommend that the proposed definition of “hybrid entity” in subsection 18.4(1) be replaced with the following:

- hybrid entity means an entity

- that is resident in a country; and

- under the laws of another country, the income, expenditure, profit or loss of the entity is treated as if it were derived or incurred by an investor in proportion to the investor’s interest in the entity.

Similarly, we recommend that the proposed definition of “investor” in subsection 18.4(1) be replaced with the following:

- investor, in a hybrid entity, means a particular entity

- that holds, directly or indirectly, an equity interest in the hybrid entity; and

- under the laws of a country in which the particular entity is resident, the income, expenditure, profit or loss of the hybrid entity is treated as if it were derived or incurred by the particular entity in proportion to the particular entity’s interest in the hybrid entity.

Partially Owned Hybrid Entities

The rules relating to hybrid entities may produce inappropriate results in circumstances where a Canadian-resident hybrid entity has multiple owners and only some of those owners are located in countries that view the Canadian-resident entity as fiscally transparent. In these scenarios, the “double deduction mismatch” in respect of a payment by the Canadian-resident hybrid entity is, under the Proposals, equal to the full amount of the payment, rather than the portion of the payment that reflects the relevant investors’ share of the hybrid entity’s income. However, the amounts included in “dual inclusion income” may be limited to the portion of the revenue amounts that are included in the relevant investors' share of the hybrid entity’s income. If the rules are interpreted in this manner, they would produce additional Canadian tax in scenarios where there is no actual hybrid mismatch.

This can be illustrated by the following example, involving a Canadian ULC (“Canco”), which is treated as fiscally transparent for U.S. tax purposes. 20% of Canco’s shares are held by U.S. residents (the “US Investors”); the remaining shares are held by Canadian residents. Canco has $50 net income, consisting of $150 of revenue amounts and $100 of deductible payments. Canco is subject to Canadian income tax on its $50 income; the US Investors are subject to U.S. income tax on their share of this income of $10. For the purposes of this discussion, we assume that the conditions in paragraph 18.4(15.5)(b) are satisfied. The hybrid payer rules appear to produce the following results:

- The $100 of deductible payments by Canco produce a double deduction mismatch, as amounts in respect of these payments are deductible in computing income for Canadian and U.S. tax purposes. Specifically, the full $100 amount of the payments is deductible in computing Canco’s income for Canadian tax purposes, and the US Investors’ 20% share of the payments is deductible in computing their income for U.S. tax purposes. Under subsection 18.4(7.2), the amount of the double deduction mismatch is $100 (i.e., the full amount that is deductible by Canco in respect of the payment, rather than the partial amount that is deductible by the US Investors).

- Under subsections 18.4(4) and (15.6), Canco’s deductions for the payments are denied, to the extent the $100 double deduction mismatch exceeds the amount of dual inclusion income in respect of Canco.

- Amounts will be included in Canco’s dual inclusion income if those amounts are both ordinary income in respect of Canada, and ordinary income of the US Investors in respect of the U.S. The ordinary income in respect of Canada is $150 (i.e., the revenue amounts that are included in computing Canco’s income for Canadian tax). The amount of the US Investors’ ordinary income is not entirely clear. Under one interpretation, their ordinary income is also $150, as they are subject to U.S. tax on their share of Canco’s net income, and the $150 revenue amounts are included in computing that net income. However, under another interpretation, the US Investors’ ordinary income is only $30 (i.e., 20% of the revenue amounts), since the US Investors are subject to U.S. tax on only 20% of Canco’s income.

- If the second interpretation were correct, Canco would have a hybrid mismatch amount of $70, which would be non-deductible under subsection 18.4(4). That would be an inappropriate result, as there is no real hybrid mismatch in this scenario: Canco has net income, which is subject to tax in both countries (rather than a net loss that can offset taxable income in both countries).

In our experience, the hybrid mismatch rules of other jurisdictions do not produce such results in partial ownership scenarios. For example, the U.K. hybrid rules limit a double deduction to the amount that is both (a) deductible from the income of the hybrid entity, and (b) deductible from the income of an investor.6 Dual inclusion income is similarly limited to the amount that is included in ordinary income of both the investor and the hybrid entity.7 The E.U.’s Anti-Tax Avoidance Directive addresses this issue in a similar manner: a “double deduction” is defined as a deduction of the same payment, expenses or losses in the payer jurisdiction and the investor jurisdiction; and “dual inclusion income” is defined as an item that is included in income in both jurisdictions.8

The Action 2 Report takes a different approach in these scenarios. Where the defensive rule applies to a hybrid entity, it denies the deduction for the full amount of a payment, even if only a portion of this amount is deductible by investors.9 However, in the partial ownership example provided in the Action 2 Report, the hybrid entity does not have any revenue amounts. If the hybrid entity did have revenue, we believe the full amount of this revenue would be included in dual inclusion income, rather than only the investor’s share of this revenue. This is implied by the statements that “The adjustment should be no more than is necessary to neutralize the hybrid mismatch and should result in an outcome that is proportionate and that does not lead to double taxation”.10 In other words, the defensive rule should only deny a deduction to the extent necessary to neutralize the mismatch (i.e., to the extent amounts that are deductible in both jurisdictions exceed amounts that are included in income in both jurisdictions).

The rules for hybrid entities should be clarified, to prevent inappropriate results in scenarios where only a portion of the equity interests in a hybrid entity are held by investors who view the entity as fiscally transparent. We believe the best way to achieve this result is to limit the double deduction to the amount that is deductible by both the hybrid entity and the investors (similar to the approach taken in the U.K. and the E.U.). Alternatively, the “dual inclusion income” definition could be modified, to more closely resemble the double deduction test in subsection 18.4(7.2) such that where an amount is included in computing ordinary income of both a Canadian-resident hybrid entity and an investor, the amount of dual inclusion income would be equal to the full amount that is included in ordinary income of the hybrid entity.

Recommendations:

- Subsection 18.4(7.2) should be revised so that, if a payment gives rise to a double deduction mismatch, the amount of the double deduction is equal to the lesser of the amounts described in paragraph 18.4(7.1)(a) and paragraph 18.4(7.1)(b).

- In the alternative, the “dual inclusion income” definition in subsection 18.4(1) should be modified, so that an amount will be dual inclusion income of a Canadian-resident hybrid entity if (1) the amount is ordinary income of the hybrid entity, and (2) all or a portion of the amount is ordinary income of an investor in the entity.

Hybrid Payer Arrangement Rules – De Minimis Exception

As a result of the broad scope of the hybrid payer arrangement rules, there may be instances where a minority investor is impacted and it is not practical to determine the amount of dual inclusion income in respect of that investor. For example, consider the private equity industry, where a hybrid entity makes a payment and has a significant number of minority investors. In this case, it may not be possible for the hybrid payer to obtain information in a timely manner (or at all) on how income earned by the minority investors from the hybrid entity is treated under their local tax laws. To address this difficulty, a de minimis exception should be considered.

Recommendation: Consider introducing a de minimis exception whereby a hybrid payer mismatch does not arise to the extent of the portion of a particular payment that is allocated to a particular investor in a hybrid entity, if that portion of the payment is less than a certain threshold (determined either by reference to a percentage of the total payment or an absolute dollar amount).

U.S. Dual Consolidated Loss Rules

The hybrid payer arrangement rules in proposed subsections 18.4(15.5) to (15.7) are premised on the ordering and priority concepts in the Action 2 Report.

For a hybrid payer arrangement involving a payment by a hybrid entity, the country in which an investor in the hybrid entity is resident generally applies its primary rule to neutralize the double deduction mismatch. If that country fails to do so, the country in which the hybrid entity is resident applies its secondary (defensive) rule to neutralize the mismatch.

This framework functions effectively when both countries follow the ordering and priority concepts in the Action 2 Report. However, unintended outcomes may arise when only one country applies those concepts, including the possibility of “double non-deduction” outcomes.

The U.S. dual consolidated loss (“DCL”) rules do not follow the ordering and priority concepts in the Action 2 Report, and there is concern about a potential lack of coordination between the hybrid payer arrangement rules and the U.S. DCL rules.

Hybrid payer arrangement rules

In general, the hybrid payer arrangement rules apply where a payment by a hybrid payer gives rise to a double deduction mismatch. A payment gives rise to a double deduction mismatch if:

- in the absence of paragraph (f) of the definition hybrid mismatch amount, an amount would be deductible, in respect of the payment, in computing the income of an entity from a business or property under Part I for a taxation year; and

- in the absence of any foreign hybrid payer mismatch rule, an amount would be – or would reasonably be expected to be – deductible, in respect of the payment, in computing the relevant foreign income or profits of an entity for a foreign taxation year.

The term “foreign hybrid payer mismatch rule” is defined as a foreign hybrid mismatch rule that can reasonably be considered to

- have been enacted or otherwise brought into effect by a country with the intention of implementing, in whole or in part, Chapter 6 or 7 of the Action 2 Report; or

- have an effect that is substantially similar to that of a provision under section 18.4 or section 12.7 that is intended to implement, in whole or in part, a chapter referred to in paragraph (a).

The language in paragraph (b) can be interpreted in more than one way. We assume it refers to a foreign hybrid mismatch rule that is substantially similar to the Canadian hybrid payer arrangement rules, which are intended to implement Chapters 6 and 7 of the Action 2 Report, rather than requiring the foreign rule itself to have been enacted for the purpose of implementing those chapters. Additional clarity in the Explanatory Notes would be helpful.

Assuming this interpretation is correct, the question remains whether the U.S. DCL rules – which are similar to the hybrid payer arrangement rules insofar as they restrict certain double deductions relating to dual resident corporations and hybrid entities, but differ in that they predate the Action 2 Report and do not address the full scope of measures contemplated in Chapters 6 and 7 of the Report – are considered to have an effect that is “substantially similar” to the hybrid payer arrangement rules.

Clarity on this issue is critical, as the application of the hybrid payer arrangement rules in situations involving the United States will depend on whether the U.S. DCL rules qualify as a foreign hybrid payer mismatch rule.

U.S. DCL rules

The U.S. DCL rules restrict loss sharing by dual resident corporations (“DRCs”) and separate business units. In general, losses may be used only to offset income of the entity that incurred them, unless the taxpayer can demonstrate that the loss cannot be used to offset income of another foreign entity.

The rules provide a domestic use election under which DCLs may be deducted against US domestic income, with a required five-year certification period and a recapture mechanism triggered if foreign use subsequently occurs.

A foreign use occurs if a DCL is used by a foreign entity to offset income treated as income of another foreign corporation for U.S. tax purposes. If no foreign use occurs, the US taxpayer can elect domestic use to deduct the DCL against domestic income.

The U.S. DCL regulations include a mirror legislation rule. Under this rule, a foreign use is deemed if a foreign jurisdiction enacts double deduction legislation restricting loss-sharing or deductibility, even if no foreign use actually occurs.11 The rule aims to prevent revenue loss to the U.S. Treasury by foreign double deduction laws. It applies when the foreign law denies the ability to share losses with affiliates or conditions deductibility on whether a deduction is available in another country.

The mirror legislation rule contemplates relief through bilateral competent authority agreements (“CAAs”) under which the United States and a foreign country put into place an elective procedure through which losses in a particular year may be used to offset income in only one country.

Interaction of the hybrid payer arrangement rules and the U.S. DCL rules

We are concerned that if the U.S. DCL rules are not considered “substantially similar” to the hybrid payer arrangement rules, unintended consequences could arise, including “double non-deduction” outcomes.

For example, assume a U.S. corporation owns a Canadian ULC that is treated as a disregarded entity for U.S. tax purposes, with the Canadian ULC making certain deductible payments.

If the U.S. DCL rules are not considered “substantially similar” to the hybrid payer arrangement rules, whether a double deduction mismatch arises will depend on whether an amount would be – or would reasonably be expected to be – deductible in respect of the payment for U.S. tax purposes.

If the U.S. corporation attempts a domestic use election, the payment would be deductible for U.S. tax purposes and a double deduction mismatch would arise. That would result in Canada applying the hybrid payer arrangement rules as a defensive mechanism. However, that, in turn, could activate the U.S. mirror legislation rule, creating a deemed foreign use that precludes the U.S. domestic use election.

If the U.S. mirror legislation denies the domestic use election, the payment would no longer be deductible for U.S. tax purposes. That would call into question whether a double deduction mismatch exists for Canadian purposes, potentially creating a complex and circular interaction between the two regimes. We are concerned that this could ultimately lead to a “double non-deduction” outcome.

Recommendations

- Provide additional clarity for the appropriate interpretation of the “substantially similar” language in paragraph (b) of subsection 18.4(7.1), including specific guidance on whether the U.S. DCL rules are intended to qualify as a “foreign hybrid payer mismatch rule”.

- To facilitate proper coordination with the U.S. DCL rules, we recommend that the U.S. DCL rules be treated as “substantially similar”. If this recommendation is not adopted, a relief mechanism will be needed to ensure that a payment by a hybrid payer does not result in a “double non-deduction” outcome. One option is to pursue a CAA with the United States, as contemplated under the U.S. DCL regulations. Given that negotiating a CAA may require significant time, interim relief would also be needed. An alternative approach is to include a specific provision in the Canadian hybrid mismatch rules addressing the interaction with the U.S. DCL rules that permits a Canadian taxpayer to elect to claim the deduction in either Canada or the United States, but not both, rather than applying the default ordering and priority concepts in the Action 2 Report. Under such an approach, if a Canadian taxpayer elects to forgo the deduction in Canada, we understand that a deemed foreign use would not be expected to arise under the U.S. DCL rules, in which case a U.S. domestic use election should remain available.

Structured Arrangements

A structured arrangement is defined in subsection 18.4(1) to include “any transaction, or series of transactions, if

- the transaction or series includes a payment that gives rise to a mismatch that is a deduction/non-inclusion mismatch or a double deduction mismatch; and

- it can reasonably be considered, having regard to all the facts and circumstances, including the terms or conditions of the transaction or series, that…

- the transaction or series was otherwise designed to, directly or indirectly, give rise to the mismatch.” [Emphasis added.]

We believe that the definition of structured arrangement is too broad when read together with the proposed definition of hybrid payer arrangement. As drafted, an arrangement that gives rise to a double deduction mismatch may be considered to be a structured arrangement even where the amount of the hybrid payer mismatch as computed under subsection 18.4(15.6) is nil, due to a dual inclusion income that completely offsets the double deduction mismatch. Under a broad interpretation of the “structured arrangement” definition, any arrangement involving a Canadian ULC that is fiscally transparent for U.S. tax purposes could be considered a structured arrangement, even whether any U.S. investors are dealing at arm’s length with the ULC, on the basis that a ULC is inherently designed to produce a double deduction mismatch. This could result in withholding tax issues for interest payments made by the Canadian ULC to arm’s length lenders, as discussed in the “Withholding Tax” section below.

Similarly, the definition of “structured arrangement”, as drafted, does not refer to the reverse hybrid mismatch amount as computed under subsection 18.4(15.2) or the disregarded payment mismatch amount as computed under subsection 18.4(15.4); it refers to all payments that produce deduction/non-inclusion mismatches or double deduction mismatches, regardless of whether those payments produce actual hybrid mismatches.

In contrast, the Action 2 Report defines structured arrangements as arrangements that are designed to produce hybrid mismatches, or whose pricing includes the economic benefit of hybrid mismatches, rather than referring more broadly to deduction / non-inclusion outcomes and double deduction outcomes. We believe the Action 2 Report’s approach to defining structured arrangements is more appropriate, as it focuses on arrangements that are designed to produce the types of tax benefits targeted by the hybrid mismatch rules. In contrast, defining structured arrangements by reference to all deduction / non-inclusion and double deduction outcomes risks catching all arrangements involving entities that happen to be treated differently under different countries’ tax laws, even when these arrangements are not designed to produce actual hybrid mismatches.

We realize that the currently enacted “structured arrangement” definition refers to payments that produce deduction / non-inclusion mismatches, rather than hybrid mismatches. However, that scope is less problematic in the context of the rules for hybrid financial instrument arrangements, hybrid transfer arrangements, and substitute payment arrangements, as those rules involve transactions that produce hybrid tax treatments. In contrast, the rules for reverse hybrid arrangements, hybrid payer arrangements and disregarded payment arrangements involve entities that are treated differently under the tax laws of different countries, without the need for specific transactions to achieve these results.

The proposed “structured arrangement” definition might be interpreted more narrowly (relying on the interpretive rule in subsection 18.4(2)), so that is applies only to arrangements that are intended to produce hybrid mismatch outcomes. However, we believe the proposed definition should be modified, to clarify its scope.

Recommendations:

- Paragraph (a) of the “structured arrangement” definition should be modified, to refer to a payment that gives rise to a hybrid mismatch amount (rather than a deduction / non-inclusion mismatch or a double deduction mismatch).

- In the alternative, paragraph (b) of the definition should be narrowed to apply only to the transactions or series that are designed to give rise to a hybrid payer mismatch amount, a reverse hybrid mismatch amount or a disregarded payment mismatch amount (or whose pricing reflects a portion of any economic benefit arising from such mismatch amounts).

Scope of the Reverse Hybrid Entity Definition

Subsection 18.4(15.1) outlines the conditions which are required to be met for a payment to arise under a “reverse hybrid arrangement”. One condition is that the actual payment is to a reverse hybrid entity in respect of the actual payment. A reverse hybrid entity is defined in subsection 18.4(1) as a particular entity who is a recipient of a payment who is not subject to tax on its income or profits under the laws of a country because those income or profits are seen as income or profits of one or more other entities, and such income or profits are not subject to tax in the hands of an entity who holds a direct or indirect equity interest (i.e., a reverse hybrid entity is transparent in a jurisdiction and is seen as an opaque entity by at least one of its investors).

A further condition for a reverse hybrid arrangement to apply is either (i) the payer of the payment and the reverse hybrid entity do not deal with each other at arm’s length, or (ii) the actual payment arises under, or in connection with, a structured arrangement. As currently drafted, the conditions for there to be a reverse hybrid arrangement do not take into account the relationship between the reverse hybrid entity and the entity who holds a direct or indirect equity interest in the reverse hybrid entity (i.e., an investor). However, the Action 2 Report recommends that a reverse hybrid arrangement exist only where all of (i) the investor, (ii) the reverse hybrid and (iii) the payer are members of the same control group.

As currently drafted, a reverse hybrid arrangement can result due to the tax treatment of the actual payment by an arm’s length investor in the reverse hybrid entity. This could lead to unintended consequences where, as an example, a U.S. limited liability company (“LLC”) or U.K. limited liability partnership (“LLP”) that is transparent for local tax purposes issues a membership interest to even one investor who treats the U.S. LLC or U.K. LLP as an opaque entity under the tax laws of that investor’s jurisdiction of residence.

The scope of the reverse hybrid arrangement rule should be modified to align with the scope in the Action 2 Report. In the alternative, similar to the hybrid payer arrangement recommendation discussed above, a de minimis exception should be considered in respect of a reverse hybrid arrangement where the payment allocated to an investor in the reverse hybrid entity is not greater than a specified percentage or a specified amount.

Recommendations:

- Subparagraph 18.4(15.1)(b)(i) should be modified such that the condition applies only if the reverse hybrid entity does not deal at arm’s length with both (i) the payer, and (ii) one or more of the investors who would cause paragraph (c) of the definition of “reverse hybrid entity” to be met.

- In the alternative, a de minimis exception should be introduced in subsection 18.4(15.1) whereby for purposes of the reverse hybrid arrangement rules, a payment to a reverse hybrid entity will not give rise to reverse hybrid mismatch amount to the extent the amount allocated to a particular investor is less than a certain threshold either by reference to a percentage allocation or an absolute dollar amount. This approach is not preferred, as it is inconsistent with the Action 2 Report’s recommendation to limit the application of the reverse hybrid arrangement rules to a control group.

Withholding Tax

General Application of Withholding Tax under the New Rules

The hybrid mismatch rules may impose withholding tax on payments of interest where a deduction is denied under subsection 18.4(4) or an income inclusion is required under subsection 12.7(4). It was acknowledged in the Explanatory Notes to the first set of the hybrid mismatch rules that the imposition of withholding tax in the hybrid context is a departure from the recommendations in the Action 2 Report.

At least in that context, it was possible to discern a policy rationale for deeming payments of interest to be a dividend subject to withholding tax. The Explanatory Notes to subsection 214(18) that accompanied the first set of hybrid mismatch rules state that withholding tax was meant to apply to situations where hybrids were used as equity substitutes to avoid withholding tax. For example, in the context of interest paid on a “hybrid financial instrument”, any deduction / non-inclusion mismatch often arises as the result of the recipient jurisdiction treating the interest payment as a dividend, and so there is some logic to assimilating the payment to a dividend for Canadian withholding tax purposes. This is conceptually consistent with the rationale for imposing withholding tax on payments of interest that are subject to the thin-capitalization rules, where excess debt is treated as if it should have been contributed to Canada as equity.

However, no similar policy rationale is readily apparent in the context of hybrid payer arrangements. Neutralizing the mismatch should be sufficient, and therefore a denial of the deduction should be the sole consequence. Consider the following example:

- A corporation resident in the U.S. (“Parent”) has a wholly-owned subsidiary (“USCo”), which is also resident in the U.S.

- USCo owns all of the shares of a Canadian ULC (“ULC”). ULC is resident in Canada for purposes of the Tax Act, but is disregarded for U.S. federal income tax purposes.

- ULC is capitalized with equity from USCo and interest-bearing debt from Parent. The ratio of ULC’s “outstanding debts to specified non-residents” is equal to or less than 1.5 times its “equity amount” at all times in the relevant year, such that subsection 18(4) will not deny ULC’s deduction for any of the interest paid to Parent. Payments of interest on the debt are regarded as interest to Parent for U.S. federal income tax purposes.12 The debt bears an arm’s length rate of interest determined in accordance with transfer pricing principles.

In this circumstance, payments of interest to Parent would be deemed to be a dividend and subject to withholding tax to the extent ULC does not have sufficient “dual inclusion income”. This result could also apply to payments of interest on arm’s-length debt. In these circumstances, it may often be the case that excess deductions arise from arm’s length payments other than the interest, including where the recipient is Canadian. Having regard to the Department of Finance’s intention that the rules are intended to apply proportionately to all deductions, it is conceivable that arm’s length payments to Canadian residents could increase the extent to which the interest in the example above is subject to withholding tax.

Whether a country does or does not recognize certain items of income seems wholly unrelated to the question of whether a particular payment should be treated as a disguised distribution of a Canadian corporation’s earnings; this should not cause interest payments to be viewed as a substitute for an equity return. In the example given, the debt is compliant with Canadian thin-capitalization and transfer pricing rules, and the interest is not assimilated to an equity return in the U.S. Furthermore, whether or not Canada requires a denied deduction/income inclusion first depends on whether the foreign country had denied a deduction under its own hybrid rules.

In addition, given the broad application of the hybrid entity rules to many common structures, “dual inclusion income” will often be required to avoid withholding tax. The rules, however, impose withholding tax when the interest is paid, and can deem a dividend to be paid at the end of the year to the extent of any accrued and unpaid interest that would be subject to the rules. In many circumstances, withholding tax could apply before a corporation’s dual inclusion income has been determined or is even capable of being determined. This is not an appropriate result, particularly in the absence of any earnings-stripping concerns.

The application of subsection 214(18) to interest paid under reverse hybrid arrangements raises similar issues. It does not seem appropriate to impose dividend withholding tax on such interest payments, since the deduction / non-inclusion mismatch arises from the hybrid tax status of the recipient, rather than hybrid tax treatment of the arrangement that produces the payment (e.g., this is not an arrangement in which payments are treated as interest for Canadian tax purposes but are treated as dividends for foreign tax purposes). We believe that such interest payments do not represent disguised distributions out of the Canadian tax system, since the recipient’s status as a reverse hybrid entity generally results from ownership by Canadian residents.

Arm’s Length Recipients

The Explanatory Notes acknowledge that the hybrid payer arrangement rules apply broadly, and, as a result, new paragraph 214(18)(b) seeks to limit deemed dividend treatment to payments “that inappropriately avoid dividend withholding tax”. This statement is concerning because it suggests that many common hybrid payer situations are attempting to inappropriately avoid withholding tax even though they are subject to all of Canada’s existing withholding provisions. As noted above, we believe that the application of withholding tax to hybrid payer situations is an unwarranted and unnecessary extension of a withholding tax policy decision that has already gone beyond the ambit of the Action 2 Report. The mischief addressed by the rules is unrelated to profit distribution or disguised payments, and is fully addressed by denying the excess deductions.

If you do not accept that withholding tax should not apply to hybrid payer arrangements, the rules need to go further to avoid withholding tax on ordinary arm’s length borrowings. Paragraph 214(18)(b) limits deemed dividend treatment to arm’s length non-residents unless the non-resident is “a party” to a structured arrangement. Neither the proposed legislation nor the accompanying Explanatory Notes describe what it means to be a party to a structured arrangement. The Action 2 Report does give some guidance on this point, stating that a person will be party to a structured arrangement where the person (or any member of its control group) was “aware of the mismatch in tax outcomes” and that a person will be a party if they have “knowledge of the arrangement and its tax effects regardless of whether that person has derived a tax advantage under that arrangement”.

We believe that this construct is not acceptable in the context of arm’s length financing transactions. It will be apparent to the advisors conducting ordinary due diligence for a lender that the borrower is a hybrid payer. Arm’s length lenders will not be accepting of any withholding tax risk that arises simply because the borrower is a hybrid entity or dual resident, or has a foreign branch. As always, any uncertainty concerning whether withholding tax is applicable will make it difficult to provide the required “will level” financing opinions, and may raise the cost of capital for Canadian borrowers (it is market practice for most lenders to require Canadian borrowers to provide a “gross-up” in respect of payments for Canadian withholding tax).

Similar concerns arise in the context of reverse hybrid arrangements and imported mismatch arrangements. The reverse hybrid arrangement rules in subsections 18.4(15.1) to (15.2), and the imported mismatch arrangement rules in subsections 18.4(15.8) to (15.95), can apply where the payer and recipient deal at arm’s length, if the payment arises under, or in connection with, a structured arrangement or a foreign structured arrangement, respectively. If subsection 214(18) applies to interest payments made under either of these rules, we believe that its scope should be limited to arrangements in which the payer and recipient do not deal at arm’s length. If that change is not made, the exception in paragraph 214(18)(b) should be extended to payments arising under reverse hybrid arrangements and imported mismatch arrangements.

Recommendations

- We are of the view that imposing withholding tax on payments under hybrid payer arrangements, reverse hybrid arrangements, and imported hybrid arrangements is inappropriate and should be removed from the proposals.

- If you disagree and withholding tax applies to hybrid payer arrangements, reverse hybrid arrangements, or imported hybrid arrangements, it should be limited to non-arm’s length recipients. Arm’s length borrowings should only be subject to withholding tax to the extent there is a participation feature or hybridity giving rise to equity treatment under the first set of the hybrid mismatch rules.

- If withholding tax may apply to arm’s length lenders, clear legislative guidance regarding what constitutes being a “party” to a structured arrangement (or foreign structured arrangement, as applicable) is required. This guidance should limit the concept to lenders that clearly and directly benefit from the planning of the hybrid structure, and should exclude lenders who simply obtain knowledge of the hybridity through routine due diligence of the borrower’s structure.

Imported Mismatch Rules

An imported hybrid mismatch arrangement can arise under subsection 18.4(15.92) if either (i) the payers of the mismatch payment and the importing payment do not deal with each other at arm’s length, or (ii) the payments arise under, or in connection with, a “foreign structured arrangement”. This parallels other rules that also apply either between non-arm’s length parties or in the context of a “structured arrangement”.

However, subsection 18.4(5) protects unrelated third parties from inappropriately being penalized by the hybrid rules in circumstances where (among other conditions) the payer of arm’s length payments cannot reasonably be expected to have been aware of the deduction/non-inclusion mismatch or double deduction mismatch arising from the payment. It would be appropriate to extend similar protections in the context of the imported hybrid mismatch arrangement rules.

Recommendation: Revise subsection 18.4(5) to replace all references to “a structured arrangement” with “a structured arrangement or a foreign structured arrangement”.

Subsection 18.4(19.2)

Residence of an entity is made relevant for various purposes in the Proposals. Subsection 18.4(19.2) provides that an entity is considered resident in a country if the entity is considered resident in that country for income tax purposes under the laws of that country.

However, this definition is not comprehensive of all circumstances. In particular, several jurisdictions impose comprehensive income taxation on the basis of conditions other than residence (e.g., domicile, place of management, place of establishment, etc.). This leads to uncertainty in the application of the residence concept in these rules.

Recommendation: We recommend that subsection 18.4(19.2) be revised to refer to a treaty-style concept of residence based on an entity being liable to taxation in a country based on an enumerated list of criteria (e.g., residence, domicile, place of establishment, place of management, etc.) or similar criteria. To ensure certainty, it would be helpful for this definition of residence to include a tie-breaker rule in the case of entities considered resident in multiple jurisdictions under local law, along the lines of Article 4(4) of the Canada-Australia Income Tax Convention (read without regard to the MLI13).

Concluding Remarks and Next Steps

We would welcome the opportunity to meet with officials of the Department of Finance Canada to discuss the issues and recommendations outlined in this submission in greater detail. Please do not hesitate to contact Ryan Minor, Director, Tax at CPA Canada at rminor@cpacanada.ca.

End Notes

1 OECD (2015), Neutralising the Effects of Hybrid Mismatch Arrangements, Action 2 - 2015 Final Report, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris (the “Action 2 Report”).

2 All statutory references are to the provisions of the Income Tax Act (Canada) (the “Tax Act”), as they are proposed to be enacted or amended by the Proposals, unless otherwise noted.

3 See the Action 2 Report, para. 126 (in the context of the disregarded hybrid payments rule), para. 198 (in the context of the deductible hybrid payments rule), and the definition of “dual inclusion income” in Chapter 12.

4 See the Action 2 Report, para. 127 (in the context of the disregarded hybrid payments rule) and para. 19 (in the context of the deductible hybrid payments rule). See also Example 6.4 in the Action 2 Report, which illustrates the mechanics for including CFC taxes in dual inclusion income.

5 Taxation (International and Other Provisions) Act 2010 (U.K. Public General Acts, 2010 c. 8), s. 259EC(6) – (7).

6 Taxation (International and Other Provisions) Act 2010 (U.K. Public General Acts, 2010 c. 8), s. 259IA(2).

7 Ibid., s. 259IB(8).

8 Council Directive (EU) 2016/1164 of 12 July 2016 laying down rules against tax avoidance practices that directly affect the functioning of the internal market, as amended by Council Directive (EU) 2017/952 of 29 May 2017, Article 2(9).

9 Action 2 Report, para. 200 and Example 6.5.

10 Action 2 Report, para. 200.

11 Further insight into what does and does not trigger the mirror legislation rule can be found in Treasury Regulation §1.1503(d), Example 18: “The Country X mirror legislation prevents a Country X branch or permanent establishment of a non-resident corporation from offsetting its losses against the income of Country X affiliates if such losses may be deductible against income (other than income of the Country X branch or permanent establishment) under the laws of another country.” This is determined to be mirror legislation, which precludes a domestic use election.

The Example then contrasts this result with the result under alternative facts: “[t]he facts are the same ... except that the Country X mirror legislation operates in a manner similar to the rules under section 1503(d). That is, it allows the taxpayer to elect to use the loss to either offset income of an affiliate in Country X, or income of an affiliate (or other income of the owner of the Country X branch or permanent establishment) in the other country, but not both. Because the Country X mirror legislation permits the taxpayer to choose to put the dual consolidated loss to a foreign use, it does not deny the opportunity to put the loss to a foreign use. Therefore, there is no deemed foreign use of the dual consolidated loss ... and a domestic use election can be made for such loss.”

12 While USCo will obtain a deduction for the payment by ULC that will offset the interest inclusion under group consolidation rules, the CRA accepts that these and similar structures are not subject to Article IV(7) the Canada-U.S. Tax Treaty, presumably in part on the basis that there is no earnings-stripping concern.

13 Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (the “MLI”).